Credit union marketing analytics are improving – but the gap between spend and insight remains significant. Social media campaigns, email outreach, partnerships, broker channels and community events are just some examples of marketing activities. But campaigns cost money and staff time. Critically, when loans arrive, there’s little insight into their origin.

As a result, it’s hard to make informed decisions about where to invest a marketing budget if you can’t connect spending to outcomes.

Connecting the dots: from source to decision

NestEgg’s Decision Engine now provides a continuous line of sight from the moment an applicant enters the journey through to the final lending decision.

NestEgg users are now able to answer important questions for the first time:

Which campaigns are working?

Campaigns need to not just drive traffic. Marketing effort should provide loans you can make. A campaign that generates volume but ends in declines isn’t a success – it’s a cost. Now NestEgg Decision Engine users know which is which.

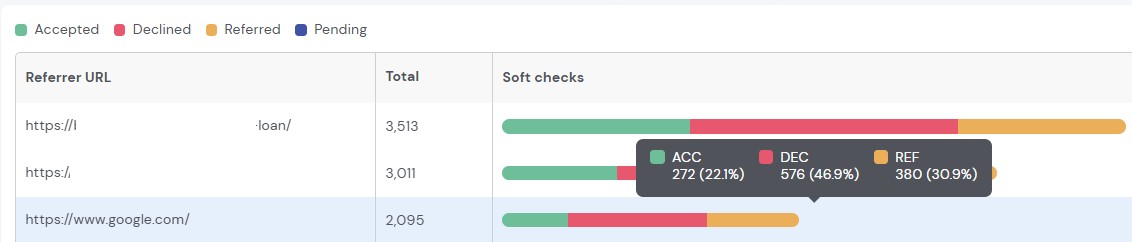

In the screenshot below we can see that Google organic traffic was the third highest referral source for the credit union. There were 3,011 visits 1,228 converting to soft checks (41% conversion). Those soft checks led to twice as many declines as accepts. This finding is an opportunity to sharpen messaging to improve the acceptance rate ahead of any paid campaign:

How Google drives traffic for soft credit checks

Where are applicants dropping out?

Drop-off happens. What matters is knowing where and when. A member who exits before starting a full application is a different problem to one who walks away halfway through. And each has a different solution. Now you can tell them apart.

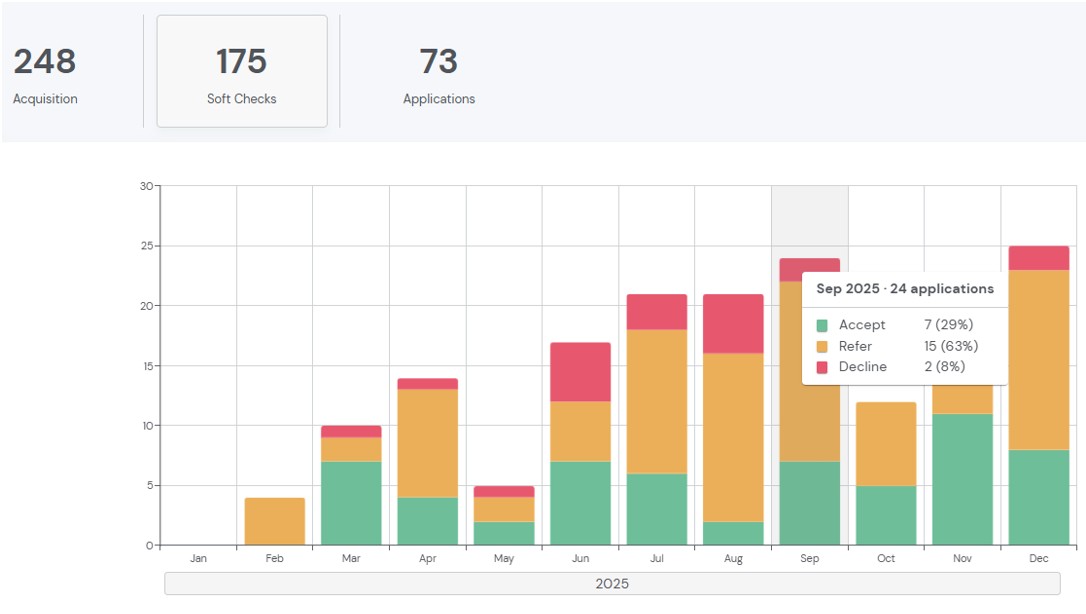

In the example below, the interest rate is doing its job. 71% of the 248 people who viewed this product went on to complete a soft check (175). That’s a strong acquisition signal. The soft check itself isn’t the problem either. Only 8% were declined, leaving 161 people qualified and ready to apply. But just 73 of them did, a 45% drop-off from qualified to completed application. That gap is the priority. 88 people cleared the eligibility bar and walked away before finishing. Next time, the credit union could try reducing the number of questions in the application to test whether friction is the cause. If conversion improves, that’s a successful experiment to repeat with other products:

Conversion rates

Does interest rate bounce have an impact?

Members dropping off when they see a higher rate is a real problem that most credit unions have never been able to measure. Until now. And if the data reveals a pattern, it provides opportunities for growth. For example, adjusting rates to reduce the proportion of people who quickly walk away. It also raises a natural question: could Risk Based Pricing convert some of those exits into loans?

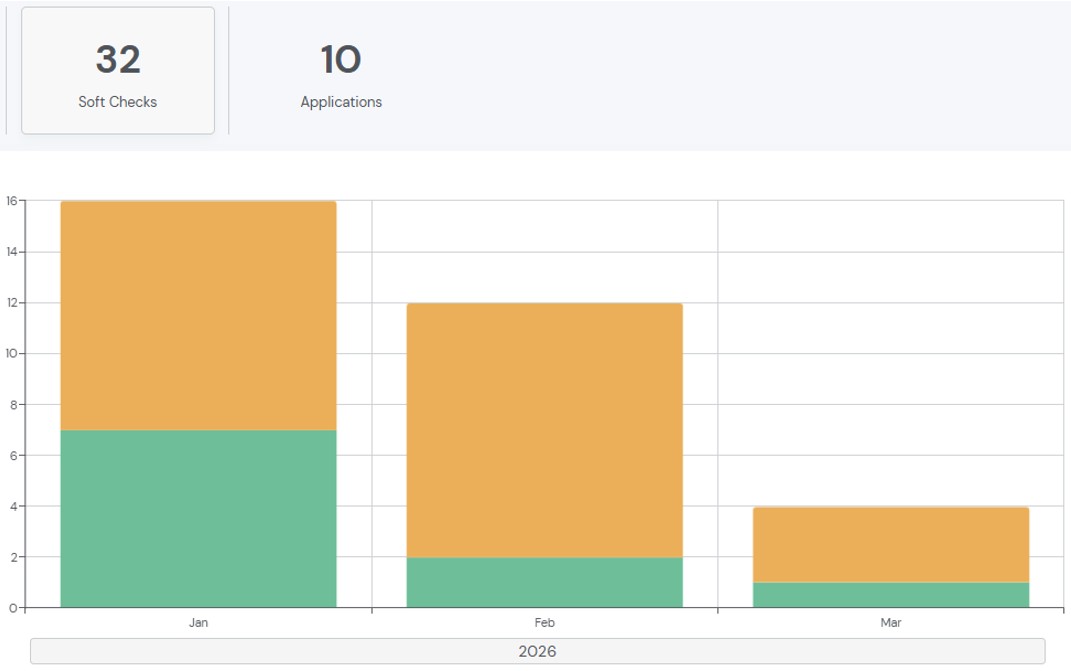

Overall this payroll loan performs well with 70% of soft checks proceeding to a full application. However when the data is filtered to good credit profiles (where borrowers are more interest rate sensitive), despite there being no declined applications two-thirds of people have dropped out. That’s double the drop out rate of people with fair credit profiles. Would Risk-based pricing help?

Good credit profile applicants not proceeding with an application

Are soft credit checks working as expected?

Soft checks are a valuable tool for letting members test their eligibility without a hard footprint. But their value depends on conversion. Knowing what proportion of members who receive a positive pre-qualification outcome then go on to complete a full application is now measurable. Better still, it can be segmented by product and credit profile.

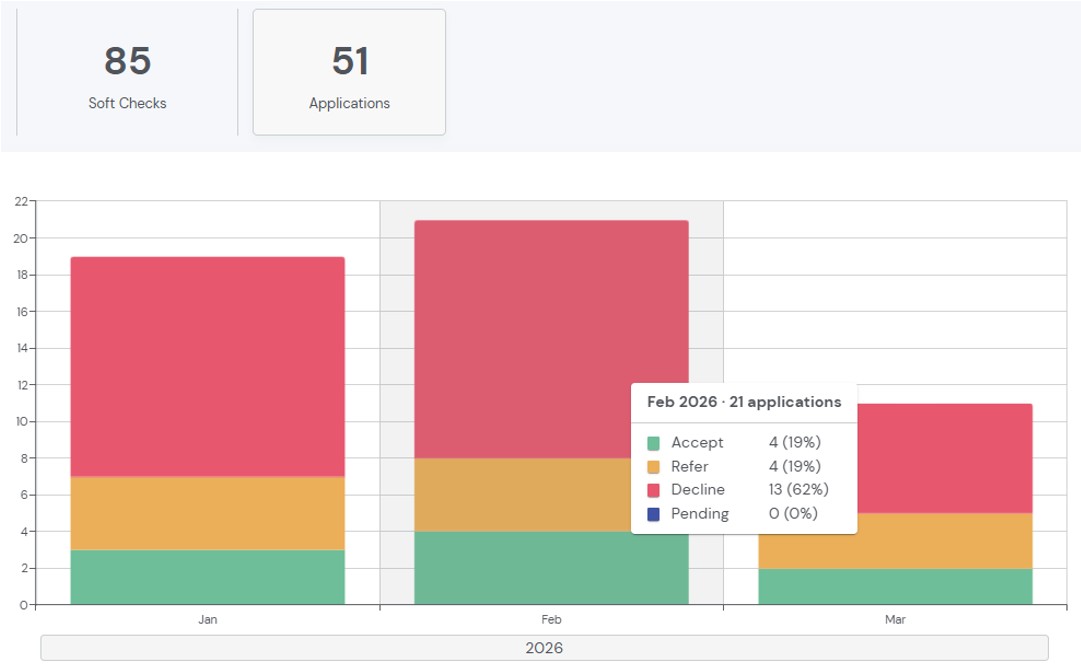

In the example below, the decline rate was 36%. Therefore, of the 85 soft credit checks, 31 were declined. As a result 54 people qualified to apply. 51 applicants actually did submit an application. Therefore the conversion rate was over 94%. Soft checks are doing their job:

The soft credit check journey

Run campaigns that actually deliver

The most immediate commercial benefit is simple: stop spending money on campaigns that don’t produce a decent proportion of accepted loans.

Picture two campaigns running simultaneously. One targets younger members through social media. The other reaches existing members with a loan renewal offer. One campaign converts at 65% and the other at 35%. Both generate 200 applications. But one drives loans you can make; the other fills your queue with applications your risk criteria can’t support.

Without referral analytics, both campaigns look broadly the same, 200 new applications enter the queue. However, with the new visibility provided by referral analytics, next quarter’s budget goes further, improving the return on investment.

Full picture, in one place

Referral analytics provides an opportunity to filter data in different ways by:

- Source or campaign. See how each acquisition tactic performs end-to-end.

- Time period. Track trends, measure campaign windows, compare periods.

- Loan product. Understand which products have higher conversion rates.

- Credit profile. Identify whether particular borrower segments are responding differently to campaigns or journeys.

The filters available for detailed analysis

The result is a single, joined-up view of your lending funnel, from the first point of contact to the final decision. The credit union team can access powerful insights in real time and improve the return on your marketing investment.

If you’d like to see referral analytics in action, request a demo below.

Book a demo now

Get insights into responsible lending

Enter your email to get insights once or twice a month

No spam. Unsubscribe anytime.