Some credit unions are processing millions in lending each year but aren’t growing at all. The reason is loan recycling. Successfully addressing this is a direct route to sustainable growth.

Why the loan recycling rate matters more than you think

The loan recycling rate measures what proportion of a credit union’s opening loan book was repaid during the year. A recycle rate of 100% means the entire book turned over in a 12 month period. As a result, the credit union had to re-advance everything it held at the start of the year just to end up where it began.

For example, a credit union with £10m on loan and a recycle rate of 80% would have to make £8m of loans just to stand still. At an average value of £1,000 this means 8,000 loans have to be issued before the loan book can grow.

Not all recycling is a problem. NestEgg’s data shows that existing members coming back to borrow are ten times less likely to default than a new borrower – making the repeat borrower one of the most valuable members in your book. The risk arises not from the top-up itself, but from refusing it. A member who is declined and seeks credit elsewhere is a very different credit risk to one whose relationship with their credit union remains intact. We’ll explore this in detail in our forthcoming White Paper topic: the Top-Up Timebomb.

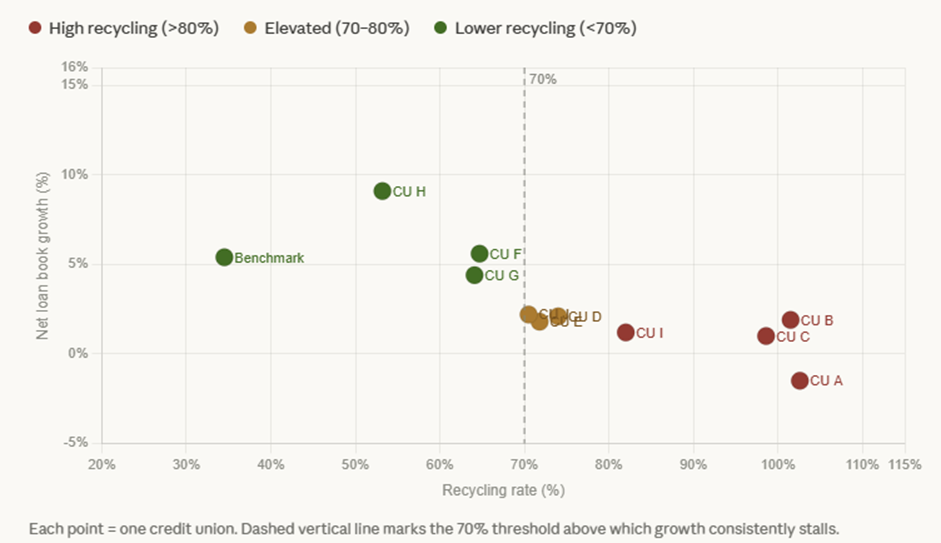

The evidence: how recycling rate predicts loan book performance

NestEgg took the public accounts of 10 credit unions with geographical common bonds to look at the recycle rate in detail. The data show a consistent pattern.

Credit unions with recycling rates above 95% achieved near-zero loan book growth despite processing enormous lending volumes. Credit unions with rates below 55% grew their loan books at up to 9% annually. They did this not by lending more, but because the money they lent stayed lent out for longer.

How to reduce your loan recycling rate: a four-point strategy

Reducing recycling is not an operational fix. Instead, it requires a shift in the profile of borrowers being attracted. The goal is members who have the creditworthiness to support larger, longer-duration loans.

Three tactics support this directly:

- Soft credit checks remove the barrier that deters credit-aware members i.e. the borrowers most likely to take a larger, longer-term loan who are concerned to protect their credit score.

- Risk-based pricing makes the credit union genuinely competitive for lower-risk members who currently find better rates elsewhere.

- Faster turnaround closes the deal: creditworthy borrowers have options, and a slow process sends them to lenders who can decide in minutes.

- Track progress using NestEgg’s powerful analytics, referral tracking and (forthcoming) Performance dashboard.

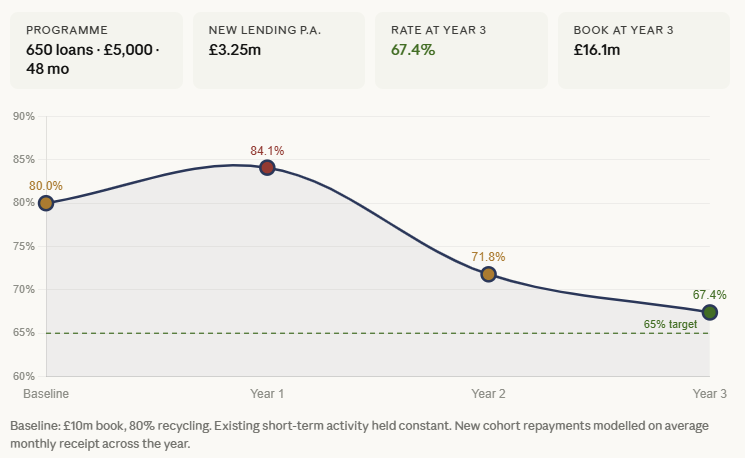

Modelling the impact: from 80% to below 70% in three years

A credit union running an 80% recycling rate on a £10m loan book can reach below 70% within three years, but it requires a deliberate shift in the type of lending being done.

The route involves introducing 650 longer-term personal loans per year – averaging £5,000 over 48 months. The recycling rate nudges up slightly in Year 1 as new advances hit the books before repayments accumulate, then falls sharply, landing at 67% by Year 3 with the loan book growing from £10m to £16m.

The critical ingredients are loan size, term length, and volume working in combination: larger loans grow the book faster, longer terms slow the rate at which repayments return, and consistent annual volume builds the cumulative effect.

The case for acting now

Loan recycling doesn’t resolve itself. Without a deliberate shift toward longer-term, higher-value lending, a credit union can remain trapped processing the same money repeatedly – active but not growing, busy but not building.

The good news is that the change required is not dramatic. A modest programme of better-quality loans, consistently applied, compounds across cohorts and moves the book materially within three years. The credit unions that address this now will be in a significantly stronger position – larger loan books, healthier income, lower operational cost per pound lent.

Book a demo now

Get insights into responsible lending

Enter your email to get insights once or twice a month

No spam. Unsubscribe anytime.