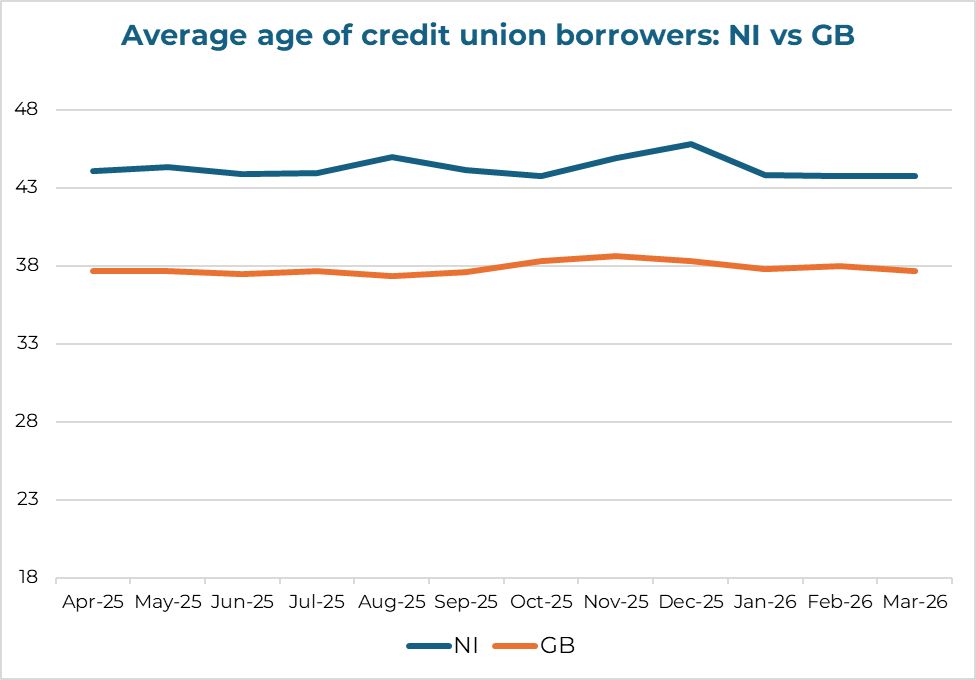

The average age of a credit union loan applicant in Northern Ireland is 44 years. In Great Britain, it’s 38. That six-year gap isn’t just a statistic; it’s a warning sign.

A membership that skews older isn’t standing still. Older members borrow less, save more, and eventually stop needing financial services altogether. A credit union that isn’t replacing them with younger borrowers is in danger of shrinking.

Thriving credit unions will be the ones that work out now how to attract people in their twenties and thirties. So why is NI running six years behind GB, and what can credit unions do about it? The data points to five clear actionable insights.

Credit scores reward age, and that’s a problem

The median age of Northern Ireland’s population is 40 years, almost identical to England’s. Therefore, demographics doesn’t explain the gap. If a credit union relies on credit scores for risk assessment, that provides part of the answer.

A borrower with a poor or very poor score is, on average, 39 years old. Applicants with a good or excellent score average 48 years. That’s nearly a decade of difference. Driven entirely by how credit scores build over time.

For example, credit scores reward mortgage holders. People with years of repayment history win more points. Therefore, a 25-year-old with stable employment and no debt will still score poorly. However, this isn’t because they’re a bad risk. Rather they haven’t had time to accumulate the evidence scoring systems reward. Applying the same credit score risk thresholds to a 25-year-old as a 45-year-old doesn’t manage risk more carefully. It may be systematically excluding younger borrowers for reasons unrelated to their ability to repay.

Actionable insight #1: Younger applicants will almost always have lower credit scores. Adjust lending rules accordingly. Open Banking affords a far more accurate picture of affordability than a score that is, in part, simply a measure of age.

The fastest credit unions are winning the youngest members

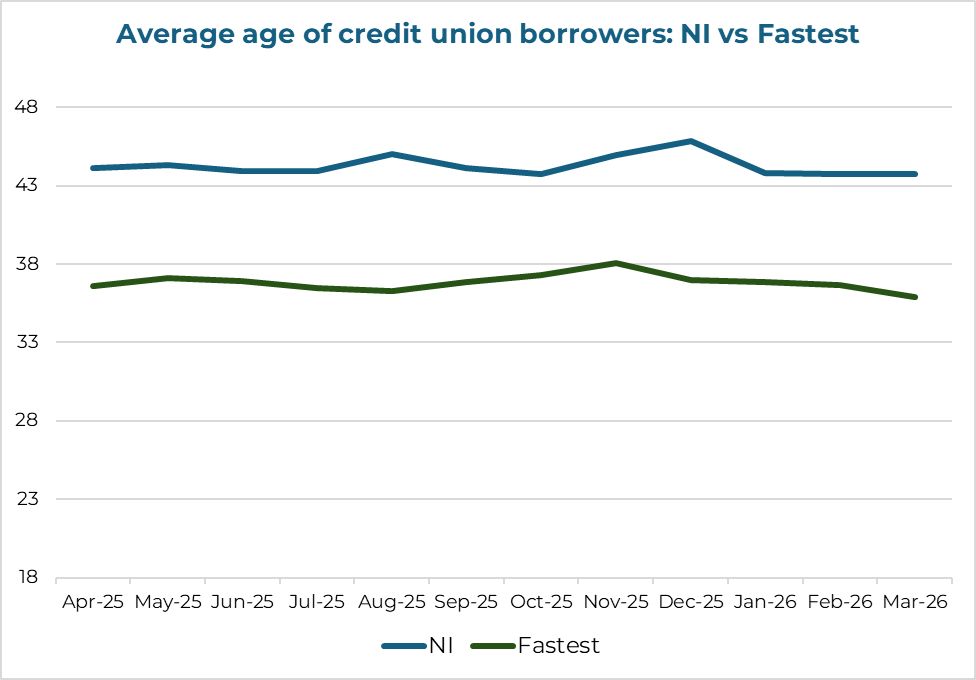

NestEgg data shows a clear link in Northern Ireland between quick turnaround times and younger applicants. Younger borrowers have grown up with instant decisions. A credit union that takes days to respond isn’t just slow, it’s signalling it wasn’t built for them.

Speed isn’t about cutting corners. It’s about removing friction. For example, replacing manual document chasing with Open Banking income verification, automated decisioning that lends responsibly, just faster.

Actionable insight #2: Turnaround time is a youth strategy. In NI, the credit unions with the fastest application journeys consistently attract younger borrowers.

Younger people borrow for different reasons, and you can market to that

Loan purpose data is specific enough to act on. Loans for study and education attract applicants averaging 35 years. Housing, including purchase, rent, and related costs has an average applicant age of 36. Debt consolidation follows at 38 years. These are the youngest segments in the data, mapping directly onto the life stages that define your twenties and thirties.

A credit union running targeted campaigns for educational and housing loans is better positioned to acquire younger members at exactly the right moment. Younger borrowers taking a loan to fund a course today, are the home improvement borrowers of tomorrow.

Actionable insight #3: Market to life stages. Study, housing, and debt consolidation campaigns will naturally pull younger members and build long-term borrowing relationships.

Urban or rural, there’s opportunity in both

Urban credit unions sit closest to where younger people live and work, yet many still post average applicant ages well above 40. That’s not a geography problem; it’s a missed opportunity. Urban credit unions should be attracting younger applicants. If they’re not, the earlier lessons on credit scoring and turnaround time may be a contributing factor.

Rural credit unions face a genuine headwind. A 43-year average age reflects demographic reality. But the variation between rural credit unions is wide enough to show that location isn’t destiny. The ones closing the gap do so through deliberate product and campaign choices: study loans for young people leaving for college, housing loans for those trying to stay in their community, debt consolidation for those looking for a fresh start.

Actionable Insight #4: Urban credit unions should benchmark against lower average age and treat any significant gap as a decisioning and digital access problem, not a demographic one. Rural credit unions should build campaigns around the loan purposes that reach younger people: study, housing, and debt consolidation.

The right products open the door

Product mix matters as much as marketing. Credit builder loans attract applicants in their mid-to-late thirties, younger than the NI average, and a genuine acquisition opportunity. But most underperform because they’re not designed with the right borrower in mind. Effective credit builder lending serves three distinct groups: young adults with thin files building from scratch, people recovering from financial difficulty and aspiring homeowners strengthening their mortgage position. Each needs a different product and different support alongside the loan.

Actionable Insight #5: Treat credit builder loans as member acquisition, not subprime rescue. Designed properly, they attract a meaningfully younger borrower and lay the foundation for a relationship that lasts decades.

Start now and close the age gap

The credit unions winning younger members in Northern Ireland are doing five things: lending on affordability not credit score, turning applications around fast, marketing to younger life stages, understanding their geography, and designing products that bring younger borrowers in at the right moment.

None of this necessitates a complete overhaul. It requires knowing where your credit union currently stands and which levers will move the needle most. NestEgg can show you your data, benchmark it against the sector, and help you agree a strategy that fits your membership and your market

NestEgg works exclusively with credit unions to improve lending decisions and member outcomes. Book a demo to see how we can help your credit union attract younger members.

Book a demo now

Get insights into responsible lending

Enter your email to get insights once or twice a month

No spam. Unsubscribe anytime.