Credit committees are built on something banks have never managed to replicate: a group of people who know their community. Who believe every application deserves a fair hearing.

That’s a genuine strength. However focusing too much on assessing individual applications misses a much bigger strategic opportunity. Credit committees with aggregated data can consider the wider loan portfolio. In doing so, they are better placed to meet member needs.

Beyond the credit file

Hesitation around credit data is understandable. Northern Ireland credit unions enjoy low delinquency rates for good reason – they know their members.

Credit scores, on the other hand, were designed in a different era for a different kind of borrower. And they can penalise complexity. For example, the member who has moved around, worked irregularly, or never needed a credit card doesn’t score well. Not because they’re a poor risk, but because the credit scoring system doesn’t forgive quickly and struggles to reward prudent financial habits.

A deeper problem is what credit data doesn’t capture at all. A credit file records debt and payment history. However, it says nothing about a member’s savings record, their assets, or the trajectory of their financial life. It can’t explain why someone fell into arrears – redundancy, illness, a family crisis – or confirm that the situation has long since been resolved.

That’s the gap a credit committee exists to fill. The story behind the data matters, and good lending decisions have always depended on someone being willing to ask for it. The challenge is building a process that surfaces that context efficiently. It also needs to make use of the wider data available to inform lending policy.

A better view of your member

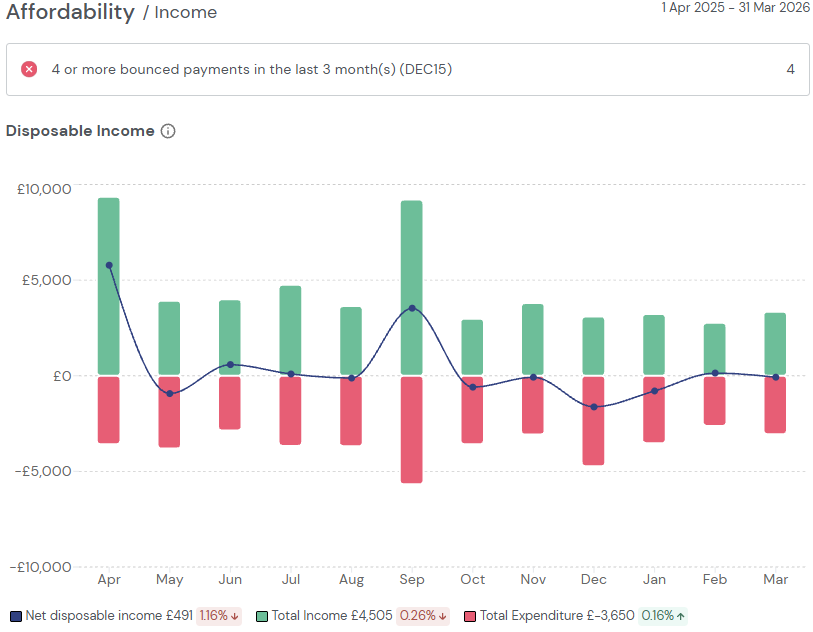

NestEgg’s Decision Engine isn’t built to determine loans by credit score. Credit scores are provided, but they sit within a holistic picture – combining credit data with Open Banking insights. This shows how a member is actually managing their finances right now. That means spending patterns, income regularity, debt-to-income ratios, and whether financial commitments are genuinely affordable (or not as in the example below):

An at a glance view of income vs expendture

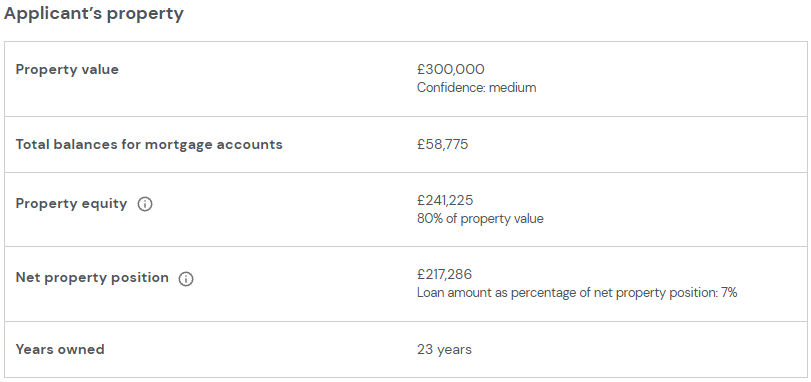

A member with a thin credit file but a stable income and sensible spending habits gets a fair hearing. However, financial health is more than the profit and loss. A member’s ‘balance sheet’ matters too. Because of this the Decision Engine also shows how much a homeowner has in equity:

View property equity and potential security for a loan

Critically, how the system is used is entirely within the credit union’s control. Credit unions can configure NestEgg so that a Loan Officer reviews every application. Over time, lenders can choose to introduce automation for clear-cut cases if they wish. But that choice always sits with the credit union. The committee’s role doesn’t diminish – it becomes better informed. Most importantly, all the data is automatically gathered in one place. As a result, the credit committee can get to work straight away.

From gatekeeper to strategist

Once committee members have better information in front of them, they can do something they have rarely had the time or tools to do: take a strategic view of the loan book.

A well-run credit union should know at a glance what its lending looks like – not just whether it’s growing, but whether it’s growing in a way that reflects its mission. NestEgg’s analytics make these questions answerable:

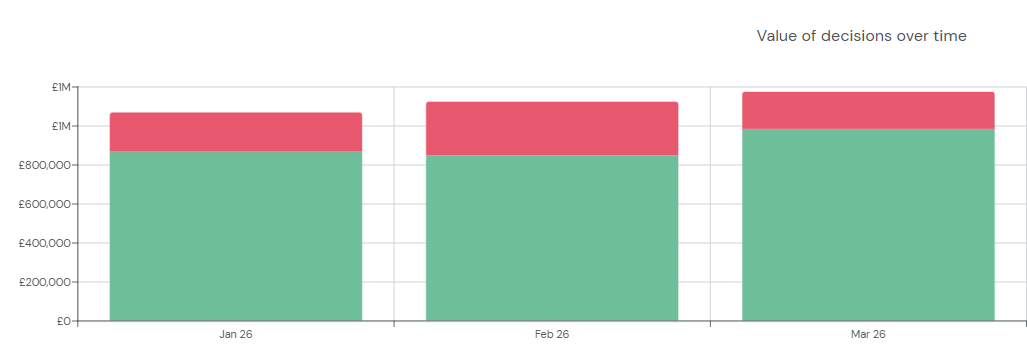

Are we growing? Lending volumes and values can be tracked daily, monthly or annually, compared against business plan targets, and used to identify whether additional effort is needed in specific areas.

Track month to month accepted and declined loan applications

How are we growing? Loan demand by purpose, by geography, and by season gives committees the insight to understand where and why lending is moving – and where opportunities exist. For credit unions with a regional common bond, geographic breakdowns can reveal untapped areas for growth.

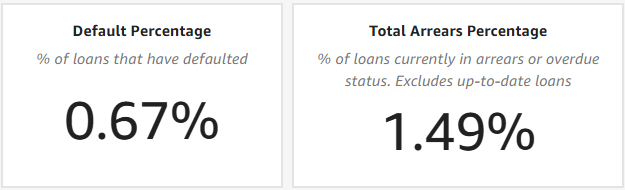

Is growth within our risk appetite? Risk Insights show bad debt rates by credit profile, loan purpose, and member type. Also, committees can see whether the balance of risk across the loan book reflects their appetite, and act before problems develop.

Review default and arrears by product and loan purpose

Review the risk of the loan portfolio, month to month

Are we supporting the right members? Tracking outcomes over time – whether approved members go on to save more, borrow responsibly, and improve their financial position – turns approval rates from a headline figure into a genuine measure of member impact.

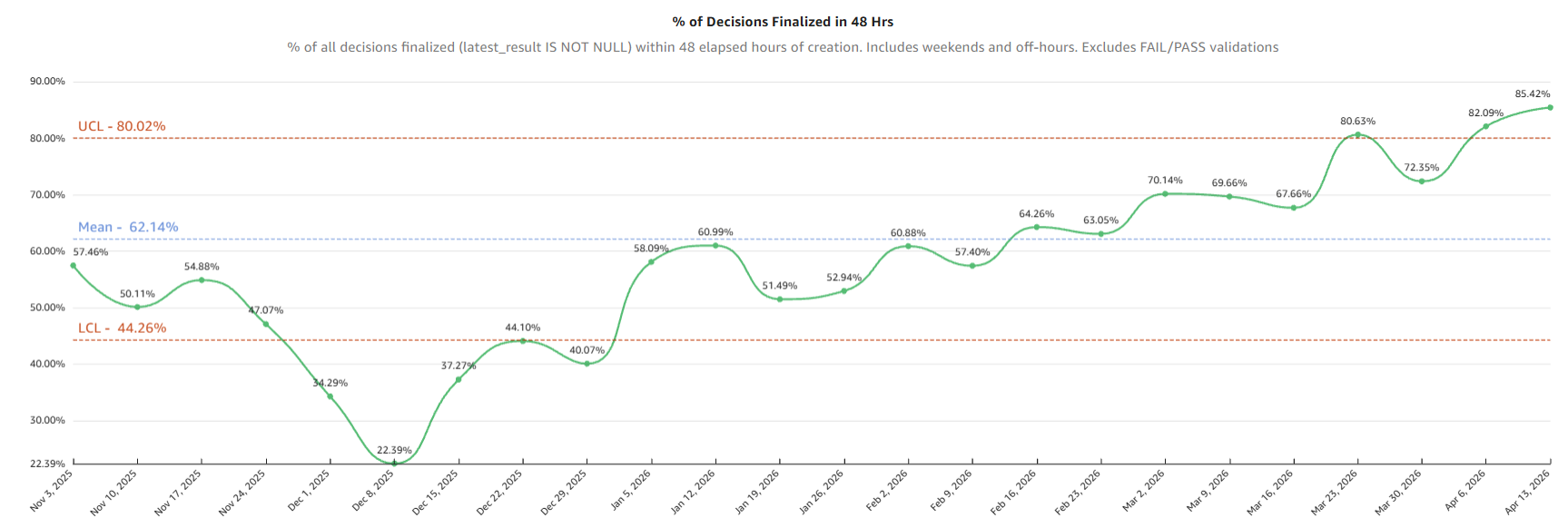

How efficient are we? How quickly are we turning loans around – and is that getting better? Fast loan decisions are essential to attract younger members.

Track how quickly loans and being turned around

This is the committee doing its job at a level it simply couldn’t reach before – not reviewing less, but understanding more.

Meeting regulatory expectations

The regulatory direction of travel reinforces this shift. The PRA’s supervisory statement on credit unions (SS2/23) is explicit that good governance means boards focusing on strategy and portfolio risk – not individual operational decisions. The regulator highlights one marker of good practice: a board that demonstrates “a clear understanding and ownership of strategy and associated risks, focusing on this as a key agenda item at board meetings (rather than getting involved in operational detail).”

The same guidance requires credit unions to maintain business plans with measurable targets for loans, savings and arrears, with progress discussed regularly, variances analysed, and corrective action taken when needed.

That is a description of a committee doing portfolio oversight with data – not one restricted to a periodic review of individual applications. The regulatory expectation and the strategic opportunity are pointing in the same direction.

Lending with heart. And rigour.

The credit committee’s instinct to see the person behind the application is a competitive advantage – and a key differentiator. Good data makes that instinct sharper.

The strongest credit committees in Northern Ireland’s credit union sector will be those who use data not to replace their judgement, but to sharpen it – and to demonstrate to members, regulators, and funders alike that lending with heart and lending with rigour are the same thing.

NestEgg’s Decision Engine combines credit reference data and Open Banking insights to support fair, fast and transparent lending decisions – designed from the ground up with responsible lenders. Request a demo below.

Book a demo now

Get insights into responsible lending

Enter your email to get insights once or twice a month

No spam. Unsubscribe anytime.