Credit builder loans can help members improve their credit score. The reality is a 15% accept rate and little improvement on scores in the short term. But the problem isn’t the product. It’s the approach.

One name, three markets

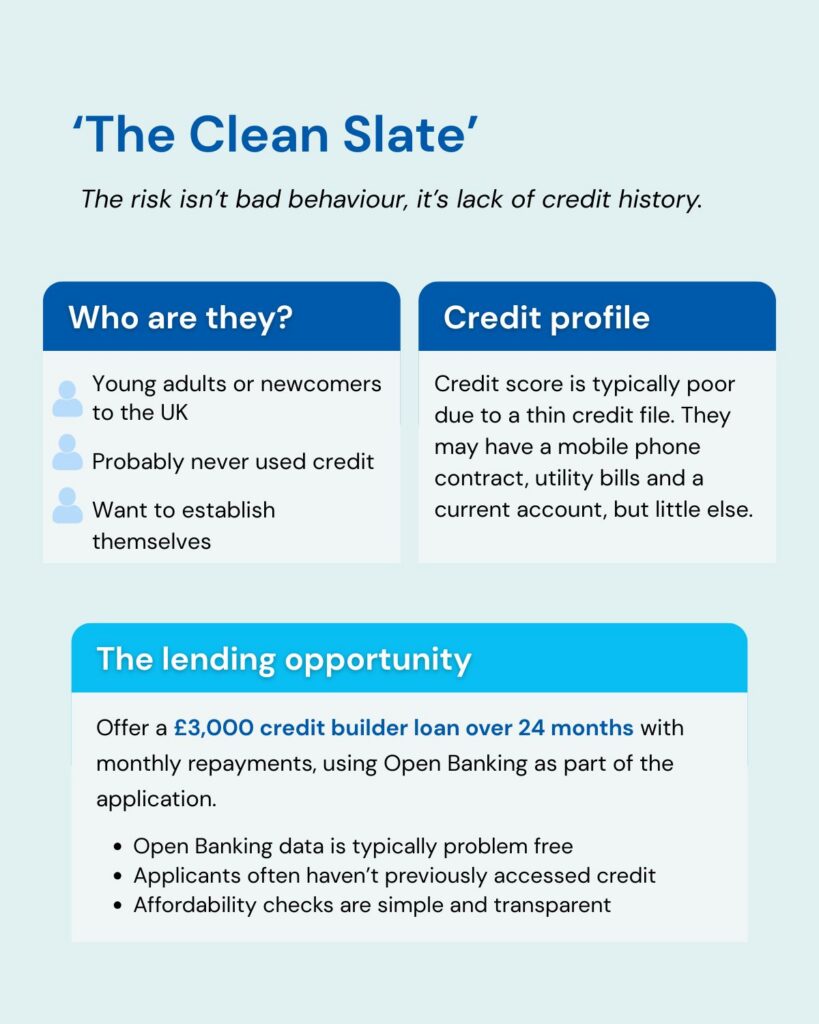

3.2 million UK adults have adverse credit history including CCJs or defaults. 1.5 million have what are known as ‘thin’ credit files. In other words, people with little or no visible history of borrowing. A third cohort (estimated at 7 million) have some credit history but an insufficient track record of borrowing. As a result, it makes it hard for them to maximise their credit score.

These aren’t the same people. But the name “credit builder” has to attract all three types of applicants. However, overwhelmingly, these are adverse credit history applicants.

NestEgg analysed over 1,000 credit builder loan applications. The typical applicant has a very poor credit score. One in four have a CCJ. One third have a default on file. Almost all applicants are at or over their credit card limits.

These aren’t thin file applicants building from scratch. Nor are they people nudging their way onto the property ladder. Rather, applicants tend to be people in financial distress who’ve confused “credit builder loan” with “bad credit loan.” In other words, a perceived higher chance of being accepted, with the credit building element only a secondary concern.

The FCA reviewed credit builder products in late 2025 and found little evidence they improve scores. CFPB research in the USA found that credit builder loans worked for people without existing debt. However, for those already over-committed, adding even a modest payment increased delinquency elsewhere.

Recommendation 1: Cater for all three audiences in marketing, screening, and product design.

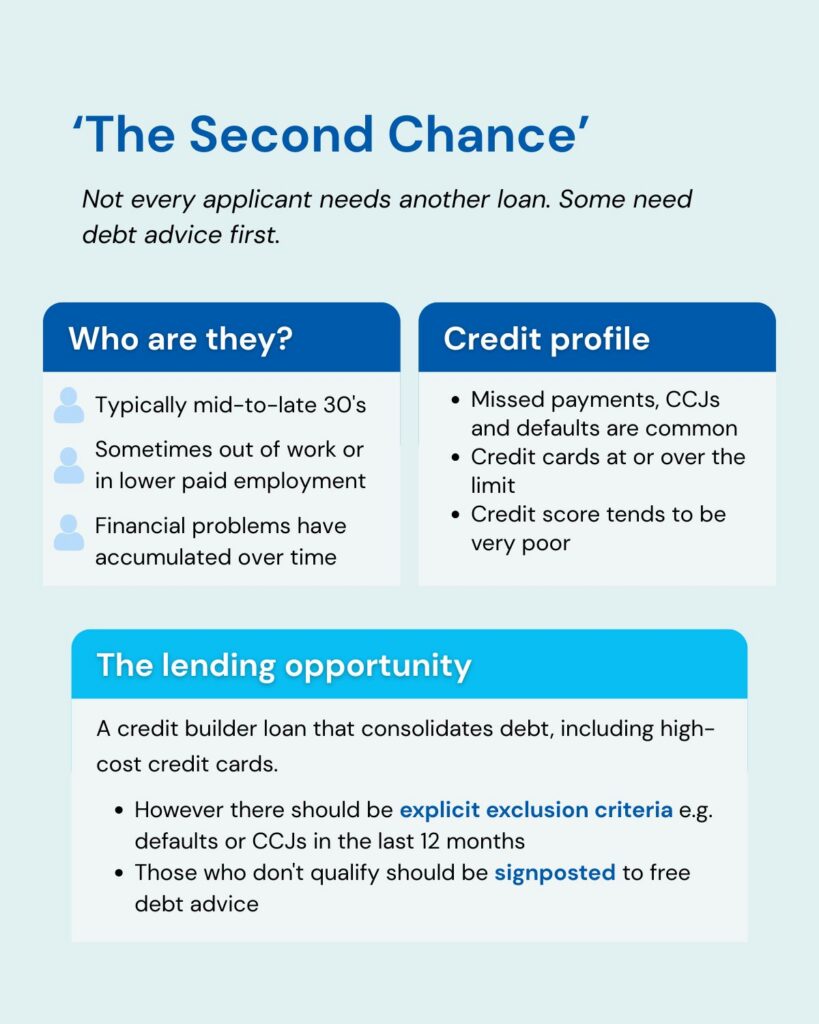

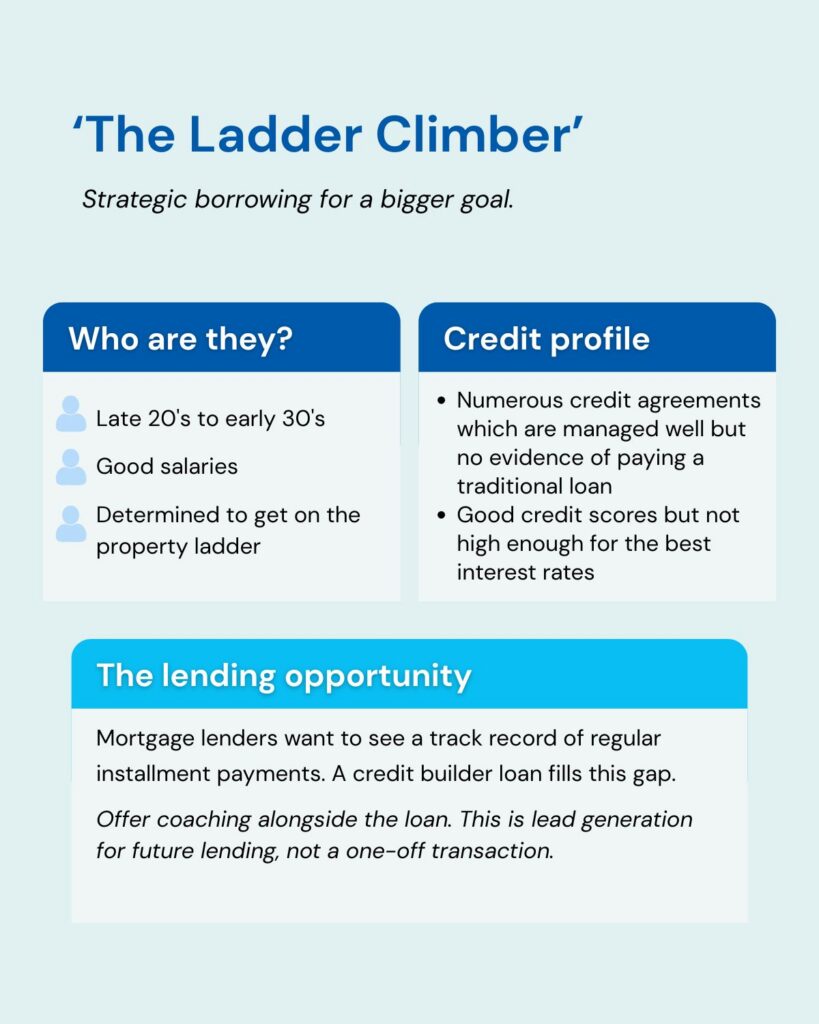

Three types of credit builder borrower

Each of these three types of borrower would benefit from a distinct approach.

Recommendation 2: Make Open Banking a requirement from the outset.

Recommendation 3: Be explicit about exclusion criteria – for example, defaults or CCJs in the last 12 months. Those who don’t qualify should be signposted to free debt advice.

Recommendation 4: Offer coaching alongside the loan. This is lead generation for future lending, not a one-off transaction.

Caution: borrowing to build… but first, a dip

Taking out a credit builder loan will initially reduce a credit score. Three things happen at once:

- Hard search. The credit check costs points and stays visible to other lenders for 12 months

- New debt. Total indebtedness increases, which lowers the credit score

- No track record. Until payments are made, there’s no evidence that the new loan is affordable.

The credit score typically recovers within a few months if payments are made on time and jumps more quickly as the debt is reduced. However borrowers need to understand this is multi-month commitment, not a quick fix.

Recommendation 5: Use soft searches to pre-qualify applicants before full application. This protects their score and improves conversion by filtering out adverse applicants early.

Then what goes down must come up

Credit scores reward evidence of responsible borrowing, reported to Credit Reference Agencies, over time. Support borrowers by providing tips (but not regulated ‘advice’):

- Make every payment on time. Payment history is key. One missed payment reduces the credit score, but 3 or more missed payments will send the rating tumbling.

- Have less than 25% of credit card limits being used. This shows cautious use of credit, boosting score.

- Pay down credit cards in full each month. A great boost to credit score, but plastic is a temptation that needs managing.

- Get on the electoral roll. Free, takes minutes, and some lenders auto-decline without it.

- Avoid multiple applications. Each hard search leaves a footprint. Pre-qualify with soft checks first.

Recommendation 6: Send tips and resources alongside any loan. But do not provide advice on why a loan is declined – that’s a regulated activity.

The strategic opportunity

Credit builder lending, done well, delivers on multiple objectives at once:

- Younger borrowers. Thin file applicants skew young. Acquire them now and they become lifetime members.

- Larger loans, longer terms. £3,000 loan over 24 months generates more income and builds more credit history for the borrower. This is the lending profile the credit union movement needs.

- Financial inclusion with commercial sense. Credit building identifies future-good borrowers before their score catches up with their behaviour. The thin file applicant who repays a credit builder loan can be supported to growth their credit score and access a much wider set of financial services. Importantly, at a lower cost.

Recommendation 7: Treat credit builder lending as member acquisition, not subprime rescue. The right applicants are an investment in future loan book quality.

Getting credit builder loans right

Credit builder loans work best when matched to the right borrower. The Clean Slate, The Second Chance, and The Ladder Climber each need different screening, different products, and different support.

Most credit unions don’t need to change their entire lending operation. And NestEgg can help credit unions focus on getting credit builder loans right. Request a demo and see how we can support your credit builder strategy.

Book a demo now

Get insights into responsible lending

Enter your email to get insights once or twice a month

No spam. Unsubscribe anytime.