Every loan application that doesn’t complete is a missed opportunity, for the member who needed credit, and for the credit union trying to grow its loan book. Withdrawal rate is the metric that captures this attrition. Critically, for many credit unions it’s quietly undermining growth in ways that don’t always get the attention they deserve.

Two types of withdrawal: One big issue

Not all withdrawals are the same. In order to reduce the loan application withdrawal rate, recognising the difference between these types is key.

Some members leave proactively. They’ve found a better offer elsewhere and made a conscious choice to go. Others drop out reactively, simply because they stopped engaging: a request for supporting documents went unanswered, a follow-up was missed, or the process just felt too slow.

The vast majority of withdrawals fall into this second category. And that matters, because reactive withdrawal is largely preventable.

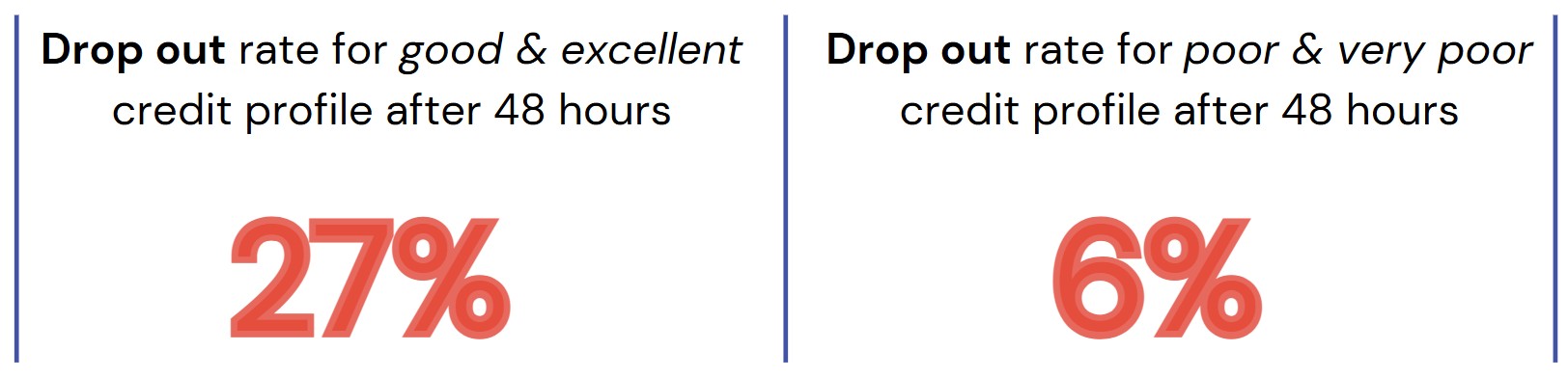

What makes this particularly striking is who is walking away. After 48 hours, 27% of applicants with a good or excellent credit score drop out, compared to just 6% of those with poor or very poor credit. Therefore, the most creditworthy members are the ones least likely to wait. They have options, and they’ll use them. Members with fewer alternatives tend to persist. The result is a portfolio that may be continuing to skew towards higher risk lending with higher running costs.

The cause: Time and follow-up

Two factors drive the majority of preventable withdrawals.

The first is turnaround time. Members apply when they need something. The longer the process takes, the more opportunity there is for life to intervene. That might be another lender responding, enthusiasm fading, or urgency passing. Speed isn’t just an efficiency gain; it’s a retention strategy.

The second is the follow-up documentation gap. Most loan applications require supporting information — a bank statement, a wage slip, proof of address. When that information arrives and sits unnoticed in a system while the loan officer is handling other cases, time passes. The member, having done what was asked of them, hears nothing. They assume the application is stalled. They move on.

Smarter alerts, Faster action

The good news is that both drivers are addressable, and technology plays a central role in solving them. Specifically, digital solutions have helped credit unions to reduce the loan application withdrawal rate in recent years.

For example, NestEgg recently released an automatic notifications feature that alerts loan officers the moment something happens on an application. When a member connects their bank account via Open Banking, or uploads a wage slip, the loan officer knows immediately, without needing to manually check.

Another feature is being able to organise loans that are likely to slip away by filtering all loans that are outstanding after 48 hours.

Importantly, turnaround time and the withdrawal rate is an output of many administrative processes. Many of these simple changes are process changes that can easily be activated by credit unions. And it’s important to remember that some of the traditional methods used by credit unions to manage bad debt have the opposite effect. For example the more paper-work heavy credit unions actually have higher rates of delinquency. Optimising these processes helps to reduce loan application withdrawal rate across the portfolio.

More engaged members, stronger growth

If your current withdrawal pattern means your best credit risks are leaving at a disproportionate rate, then addressing withdrawal will naturally improve the profile of your completing applicants. Fewer write-offs, better outcomes, and a loan book that more accurately reflects the quality of your membership.

Join Us: Lunch & Learn on Withdrawal Rate

On 11 March at 12:30, we’re running a dedicated Lunch & Learn webinar focused entirely on withdrawal rate: what’s driving it, what credit unions are doing to reduce it, and what the data tells us about where to focus. This session will provide strategic guidance to help you reduce your loan application withdrawal rate.

It’s 30 minutes, it’s free and we’ll be sharing real examples from credit unions that have already made meaningful progress on this metric

Book a demo now

Get insights into responsible lending

Enter your email to get insights once or twice a month

No spam. Unsubscribe anytime.