Good data means better loan decisions. With 100s of data points flowing through our software, the potential for credit unions to strategise lending is unprecedented.

Because of this we’ve enhanced our lending analytics. Additionally, they’re provided as standard with our Decision Engine. Lenders can take a step back from individual loan decisions and consider the risk of their overall portfolio.

This new feature is now available to all existing and new clients at no additional cost.

Here’s a snapshot of just two of the charts we provide.

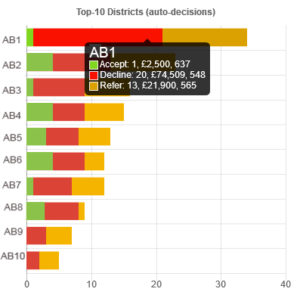

Loan decisions by district

A lender might be running a marketing campaign in a neighbourhood. Analytics show the proportion of accept, refers and declines, together with average credit score by postcode area.

Charts show places where applications originate. Number and value of loans are displayed. Different time periods can additionally be revealed.

Credit score and historical data contributes to understanding likely bad rates by postcode area. Lending focused in one area demonstrates concentration risk.

Compared to the average, a higher proportion of refers and accepts suggests the communities from which you are receiving applications align with product and risk appetite.

Because of this, lenders can now better align marketing campaigns with risk appetite.

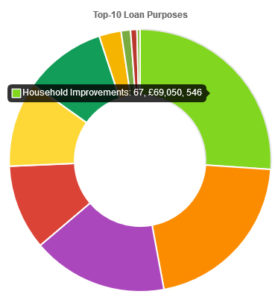

Top-10 loan purposes

Some types of loan application result in lower credit scores and higher bad rates.

Emergency loans may have lower scores than wedding applications. Consequently marketing strategy will focus on bigger loans helping people get married. Lenders might time marketing campaigns for when applications are better quality if this varies over the year.

Homeowners targeted by marketing should result in more accepts for home-improvement loans. If the aim has been achieved, lending analytics show this.

Car loans may result in better applications. Lenders over-budget for bad debt can focus effort on this product because it produces fewer write offs.

What else?

Think historical trends. Also tracking marketing campaigns that deliver more accepts. Managers can run ‘retro analyses’ to review bad debt. And much more.

Additionally, we can build custom analytics dashboards for your unique circumstances, e.g. to combine decision data with 3rd-party marketing, CRM and core systems data. Contact us to discuss if this may be of interest.

Get in touch for a demo.

Book a demo now

Get insights into responsible lending

Enter your email to get insights once or twice a month

No spam. Unsubscribe anytime.